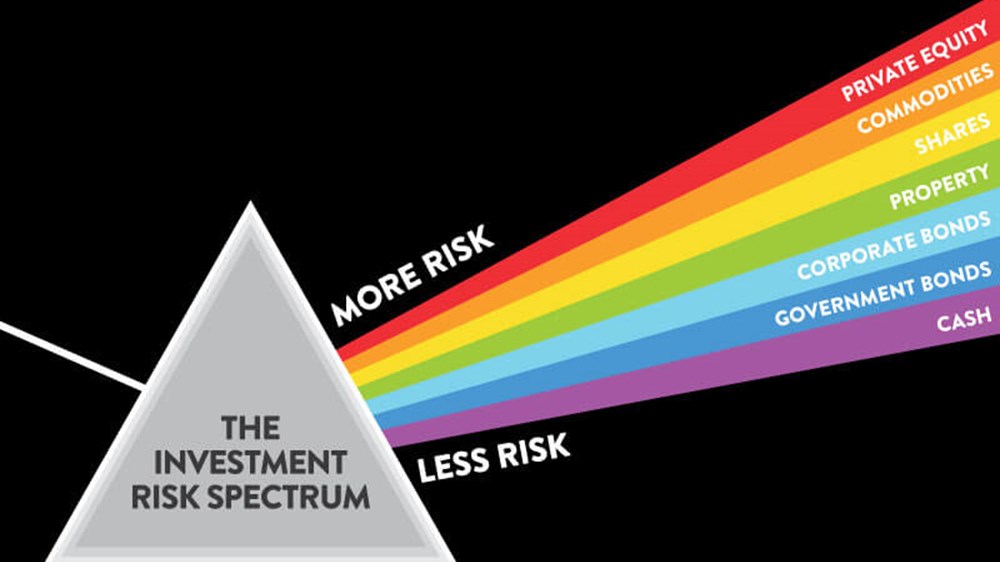

Your Wealthify Plan contains many types of investments, depending on the level of risk you’ve chosen. Bonds are among the products we buy for you, so to understand more about them here’s an overview of what they are and where they stand on the risk spectrum.

What are bonds?

Bonds are investment products created by governments and companies to raise money to pay for significant projects, like transport and energy infrastructure, or a new factory and capital equipment. When you buy a bond, you are essentially lending money to fund these activities. In return, you get a promise you’ll get your money back, plus a bit of interest to make it worth your while.

A bond is one of the better-known types of investment, possibly due to their broad availability and appeal as an easy route into investing. Bonds are typically considered a low-risk investment, and usually take their place above cash and cash equivalents on the risk spectrum – but why?

How do bonds compare to shares on the risk spectrum?

Like people and places, investment types have unique characteristics which distinguish them from each other. So, what are the main differences between a bond and a share (a portion of ownership of a company)?

Set investment time: bonds can have an end date, at which point the government or company should repay the investor. In contrast, shares have no set investment time, you could keep your money in there indefinitely or take it out whenever you like. Put simply, investing in bonds is like watching a 2-hour film – you know when it will end – whereas shares are more like watching Coronation Street, which never reaches a conclusion and it’s up to you when to stop watching.

Interest payments: when you buy a bond, you can receive interest payments (aka yields). Also known as coupon payments, interest payments are typically paid quarterly, semi-annually or annually, and can either be fixed or floating rate or inflation-linked. Fixed interest payments are agreed when the bond is issued and will vary between bonds. Floating rate bonds have a rate which mainly follows market interest rates. Inflation-linked interest payments are linked to an index of inflation. In each case, remember that bonds don’t guarantee payments since there is a risk that companies and governments can default, and you can receive less than your initial investment. With shares, there are no agreed interest payments. Shareholders may receive a dividend but that isn’t guaranteed and mostly depends on each company’s financial circumstances.

Promise of loan repayment: when you hold a bond, you would typically be repaid in full after your investment reaches its maturity date. However, there is no certainty you will get back what you originally paid in. If a company goes bankrupt or a government defaults, you’re likely to receive less than your initial investment. Similarly, with shares the value of your investment can go down when markets are performing negatively.

Built-in safety net: with some bonds, if a company is unable to pay back its investors, they might recoup some of their money by taking possession of the company’s equipment, property, or something else of value as repayment for the loan. These types of bonds are known as secured corporate bonds. There is no version of this for government bonds, but it’s very rare that government defaults occur. In the unlikely event a government does default, it would usually just delay repayment of the bond, or offer a reduced repayment. With shares, there is nothing secured against the original value of your investment.

Priority: bond investors have priority over share investors when it comes to getting their money back, should a company cease to exist or go into liquidation. Bond investors get paid ahead of share investors who only get their money back if there is anything left over. In fact, shareholders are at the very end of the queue when it comes to receiving consolation payments when a company is wound up.

On the whole, bonds tend to present less risks than shares, however this typically means bond investors settle for lower potential returns. The choice for investors is whether to stick to the reassurance of a fixed return, or ride the riskier rollercoaster of share prices for the possibility of higher returns. Although it’s not always the case, as a general rule the greater the risk you take, the greater the potential return.

Please remember the value of your investments can go down as well as up, and you could get back less than invested.