Managed Personal Pension

An award-winning managed Personal Pension, built around your retirement.

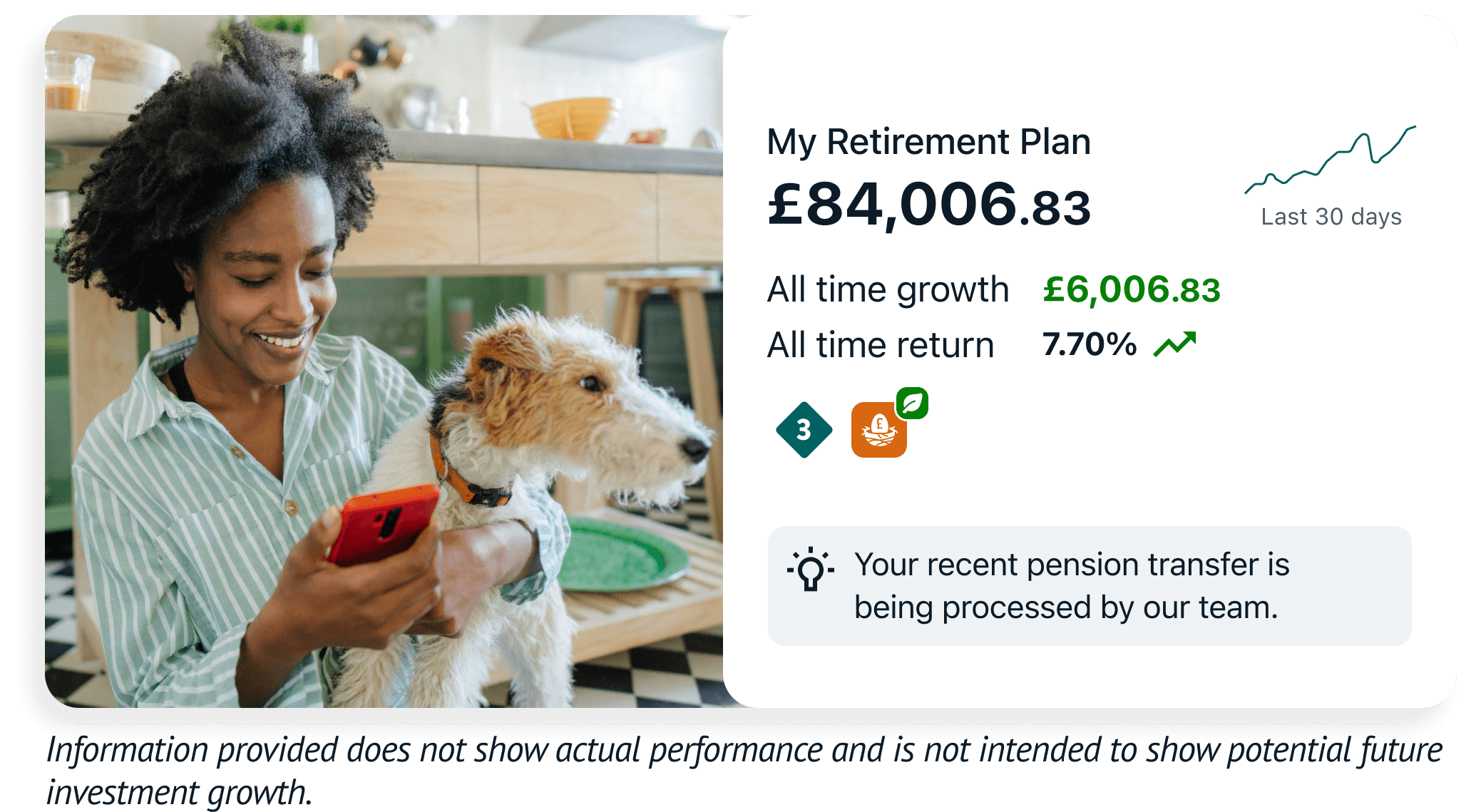

✓ A managed Personal Pension Plan that handles all the investing for you, so you don't have to think about it.

✓ Receive automatic tax relief with a 25% top-up on personal contributions.

✓ Track your retirement outlook and see how small adjustments could make a big difference.

Transfer in your old workplace pensions or start a new Wealthify Personal Pension with a £5,000 opening deposit.

With investing, your capital is at risk. Tax on your investments will depend on your individual circumstances and can change.

How to open a managed Personal Pension

Three simple steps. That’s all it takes to open a new managed Personal Pension with Wealthify.

Choose a Plan

From Cautious to Adventurous, Original or Ethical; start by telling us what type of investor you want to be.

We invest

Once we’ve established your investment style, our experts will build your Personal Pension Plan with just the right mix of investments.

We optimise

Then leave all the heavy lifting to us, as we monitor your Pension Plan and adjust it to keep your retirement on track.

Our awards

Is a managed Personal Pension right for you?

✓ You'd rather leave the investing to our experts

✓ You want your portfolio rebalanced automatically, without lifting a finger

✓ You want to build your pension pot without it taking up your time

✗ You enjoy researching the markets and picking your own stocks

✗ You already have a clear investment strategy in mind

✗ You want to react to market movements and invest on your own terms

Why choose Wealthify for your pension?

Backed and owned by Aviva, we’re trusted by over 140,000+ customers to look after their savings and investments.

Simple

You don’t need any previous investing experience with a managed Self-Invested Personal Pension (SIPP). Simply choose your investment style and track how your pension pot performs over time.

More control

Whether via Direct Debit or one-off payments, you can pay into a Wealthify managed SIPP when it suits you, helping you to build a pension pot on your terms.

Great value

One simple annual management fee of 0.6%, which drops to 0.3% for any portion that's £100,000 or above. Fees are calculated based on the value of your investments and deducted automatically each month.

Managed for you

Our Investment Team manage and optimise your investments. This includes your 25% tax relief top-up on personal contributions, which we’ll automatically add to your pot and invest for you.

Essential tools

Use our pension calculator to give you confidence over where you are with your pension, and how changes you make might affect how much your pot could be worth when you retire.

Support

Sometimes you just need to speak to an actual human being — that's why our award-winning Customer Care team is always here to help (please note, they're unable to give any financial or product advice).

Transferring a pension to Wealthify

Looking to transfer an old pension to a Wealthify SIPP?

Perhaps you have a handful of old workplace ones you’ve been wondering what to do with? If this sounds like you, then the good news is that transferring them is an equally simple three-step process, as we do all the hard work for you. And, with all your old pensions consolidated, your investments could build as one larger, combined amount!

Find your old pensions

Start by telling us a few details about your old pensions via an online transfer form, including a reference number and recent value.

The transfer process

We'll then talk to your provider(s) and start the transfer process, which usually takes within 30 days to complete.

Pension calculator

Figuring out how much you might need in retirement can feel like the hardest part of getting started — but it doesn't have to be. Our free pension calculator does the hard work.

Just tell us your name, age and expected retirement age, any pensions you're looking to transfer, how you'd like to add to your pot, and the type of investor you are (Cautious to Adventurous) and we'll do the rest. Tweak the figures to see how even small changes could affect your outcome.

Managed Personal Pension fees

When saving over long periods of time, fractions make a difference. Sure, an extra 0.01% per year might not seem like much now. But over a lifetime, that small number could add up to a big one, essentially eating into your retirement savings.

Fees cover everything we do, including setting up your account, looking after your money, and optimising your investments. Unlike some traditional providers, we won’t charge you for depositing or withdrawing money, transferring funds, or closing your Plan.

With investing, your capital is at risk. The tax treatment of your investment will depend on your individual circumstances and may change in the future.

Our reviews

SIPP FAQs

A Self-Invested Personal Pension (or SIPP, for short) provides two main tax benefits:

- You don’t pay capital gains or income tax on your investments as they grow

- You'll get an instant tax relief top-up of 25% on personal contributions.

You pay your own money into a SIPP, and can adjust how much you pay in, making it a popular option for self-employed people looking to make personal contributions — and those looking to have more than just their workplace pension for retirement.

A Wealthify SIPP will typically be invested in a wide range of investments, including shares, bonds, and property. However, it slightly differs from a standard SIPP, as our team of investment experts manage your portfolio for you.

Currently, there’s no limit on how much you can pay into your pension (although a minimum deposit of £5,000 is required), however, you won’t receive tax relief on anything over £60,000 or 100% of your salary, whichever is lower. The £60,000 limit includes all payments, including the government top up and employer contributions – so it is actually £48,000 of your contributions, plus £12,000 tax relief.

If you go over this limit you won’t receive tax relief and will have to pay an annual allowance charge which will be added to the rest of your yearly taxable income.

If your income is less than £3,600 a year, you will only be able to contribute up to £2,880 with tax relief. You can make further contributions but will not be not entitled to tax relief on them.

The following initial minimum deposits apply to each of our investment products.

Junior ISA: £1,000

Stocks and Shares ISA: £1,000

Personal Pension: £5,000

General Investment Account: £5,000

After opening your account, you can top-up (via one-off or regular monthly payments) a Junior ISA, Stocks and Shares ISA, and General Investment Account with £1 or more; Personal Pension payments need to be at least £50.

You can access your pension when you turn 55 (rising to 57 in 2028). Subject to current pension rules, you'll be able to withdraw 25% of the total amount tax-free, with the rest being taxed based on your individual circumstances. However, you don’t have to take any of your pension if you don’t want to. If you’re still working, for example, you can leave the money in your pension – and continue to contribute – until you retire.

The way you take your money out of your pension (a process known as moving your pension into drawdown), will vary depending on the type of pension you have.

If you have a defined benefit pension, you will receive a specific income for life, which should increase every year. If you have a defined contribution scheme, then you’ll be able to choose how you want to withdraw your funds using one of the following methods:

- Take your whole pension in one go as a lump sum.

- Withdraw money whenever you need it.

- Receive a regular income.

One of the easiest ways to trace old pensions is to use the government’s online Pension Tracing Service.

To use this service, you’ll need either the name of an employer or pension provider, as it can’t tell you whether you actually have a pension, or its value.

Once you’ve agreed to the service’s declaration, it’s then just a matter of answering a few simple 'yes’ or ‘no’ questions, including:

- Are you looking for an NHS, civil service, teacher or armed services pension?

- What type of pension are you looking for?

- Do you know the name of the employer, who set up your workplace pension?

- Do you know the name of your workplace pension scheme?

Wealthify automatically adds the 25% top up when you make a personal contribution to your pension and only if you ticked the box to state your eligibility for tax relief when you opened the SIPP. So, if you personally pay in £1,000, the government adds another £250, making the total £1,250. However, if you’re a higher-rate taxpayer, you may be entitled to more, in which case you will need to contact HMRC to be able to access higher-rate tax relief. This will need to be submitted on your annual tax return.

When you open a SIPP with Wealthify, you must tick the box to say you are eligible for the tax top-up. We then automatically add the 25% top up to your pension when you make personal contributions. This means we do all the work for you and you don’t need to claim anything yourself. However, if you’re a higher-rate taxpayer, you’ll need to contact HMRC for tax relief at the higher rate.

You can transfer most types of pensions to Wealthify, apart from:

- Pensions with safeguarded benefits, such as those with a defined benefit (DB), guaranteed annuity rate (GAR), guaranteed minimum pension (GMP), or final salary promise;

- Pensions with protected benefits such as Protected Tax-Free Cash, or Protected Pension Age*;

- Pensions you’re already taking an income from;

- Overseas pensions, including Qualifying Recognised Overseas Pension Schemes (QROPS);

- Crystallised plans.

Please note we can only accept defined contribution plans that have no safeguarded benefits or guarantees.

*Exception: if your pension has a protected Normal Minimum Pension Age (NMPA) of 55 or 56, we can accept the transfer.

No, unfortunately, we’re not able to accept pensions that are already in payment or if you’ve already taken income from.

Yes, however you can't pay into your Wealthify Pension from your business account. Instead you must pay from the personal bank account registered to your Wealthify account.

A personal pension can be great for sole-traders, freelancers, contractors, seasonal staff, directors in limited companies and more. Thanks to the flexibility of contributions, you can add to it when it suits you and change or pause your payments at any time using our app or online dashboard.

Take control of your future finances by starting a Self-Invested Personal Pension today.