It’s been five years since we officially launched. Whilst this is an achievement to celebrate, this key milestone in our journey also means we can now proudly present the all-important five-year performance results across each of our five investment styles for our Original Plans.

Figures in this blog are based on past performance and is not a reliable indicator of future results.

Our five-year performance

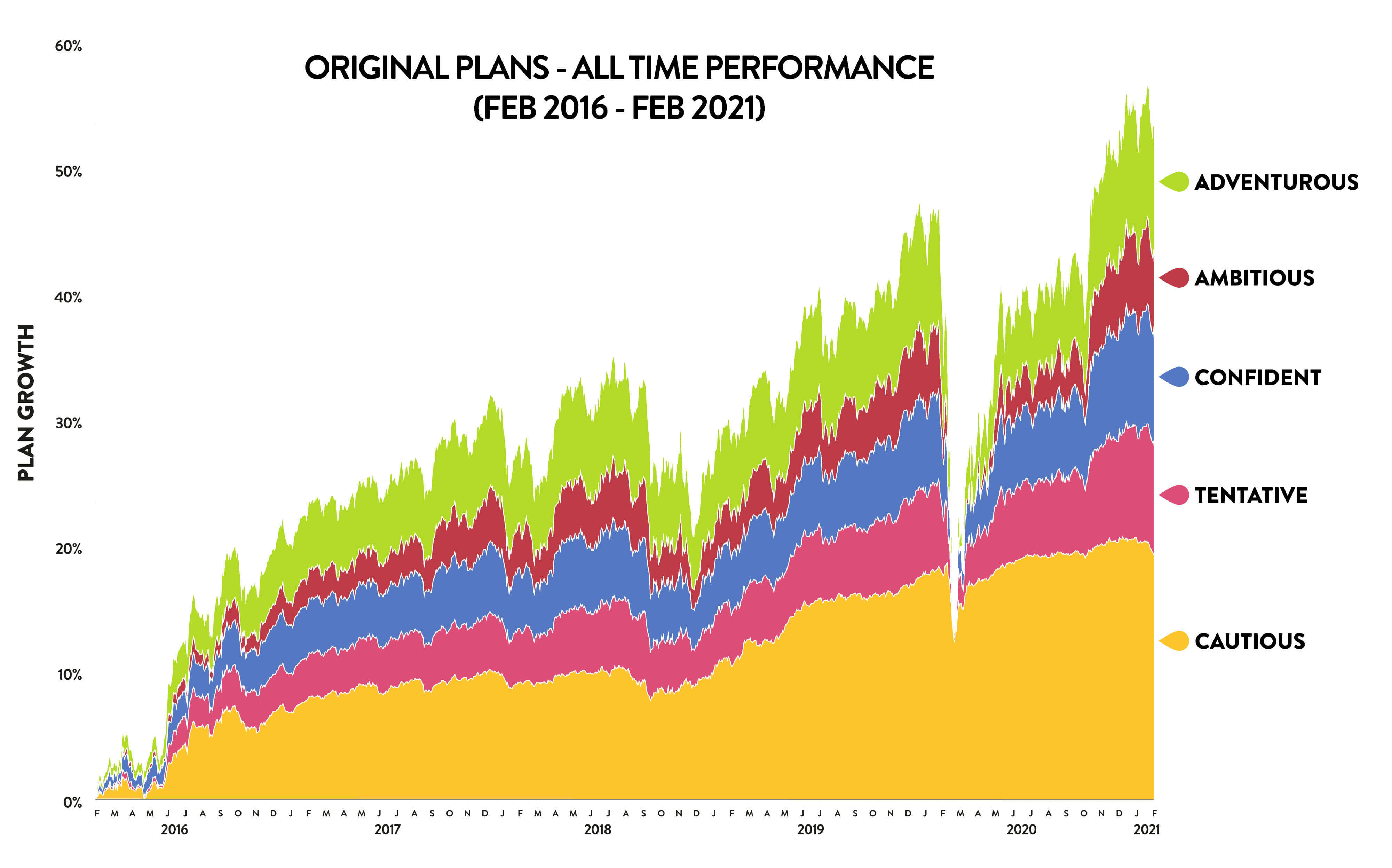

The graph below shows the simulated* performance of our Original Plans since they started, after all fees have been taken. Please note that we periodically update our performance numbers on our ‘Why invest’ page.

Over the last five years, our Original Plans posted strong, double-digit returns, and after many periods of ups and downs as illustrated in the graph below, we’re proud to confirm that our top-performing Plan (Original Adventurous) has enjoyed an overall performance of 47% at the end of the five years.

Performance breakdown

The table below shows our simulated* annual performance figures for our Original Plans, from Cautious to Adventurous, between February 2016 and February 2021, after all fees have been taken.

All-time Ethical performance

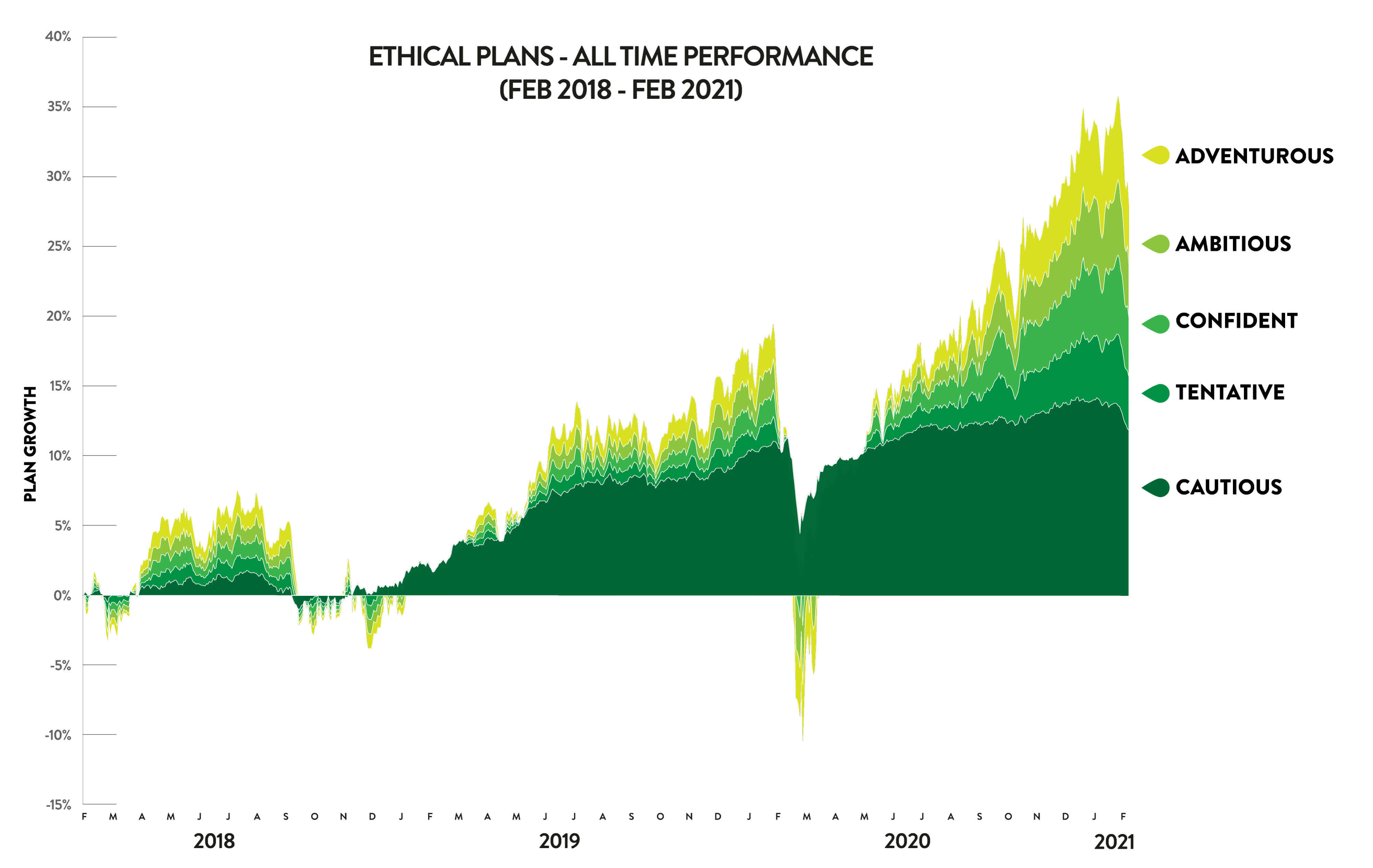

The graph below shows the simulated* performance of our Ethical Plans, since they started (February 2018), after all fees have been taken.

How did the markets perform over the past five years?

A lot happened in the last five years: the UK left the EU, Donald Trump served one term as the President of the United States, then in 2020, Covid-19, a new deadly virus, spread across the globe, forcing governments to impose national lockdowns to save lives.

Needless to say, stock markets have gone through a number of highs and lows since 2016. And if you look at our performance graphs above, you’ll see an important dip at the start of the global pandemic, between February and March 2020. This was a challenging time for markets, with many falling abruptly – for instance, between January and March 2020, the FTSE 100 lost 33.8% of its value1. But as governments and central banks announced exceptional measures to lessen the impact of Covid-19 on the economy, markets bounced back – which is reflected in the performance of our Plans.

If anything, these last five years are a reminder that investing can be a bumpy journey and is better approached with a long-term vision. Stock markets are like roller coasters – they go up and down, and there’s no way to predict where they’re heading next. We understand that it can be nerve-wracking to see your investments go down in value from time to time, but as an investor, it’s important to learn to live with the short-term bumps. And remember that historically markets have always bounced back, and in the long run, investing tends to pay off. If you invested in the FTSE 100 for any 10-year period between 1986 and 2022, you would have had an 88% chance of making a positive return – this timeframe includes many crashes, such as Black Monday (1987), the Global Financial Crisis in 2008-09, and Covid-192.

The Wealthify approach

For the last five years, our dedicated Investment Team worked tirelessly to optimise the performance of your Plans, making the necessary adjustments to your portfolio to take advantage of the good times and shelter your investments from the bad. We will continue to do so to ensure your money works as hard as it can. Whatever happens, you can rest assured that our team of experts are ready to act in your best interests and prepared to make changes to your Plans, if needed, to protect your money and provide you with higher returns.

We’ll keep in touch about any changes we make to your investment mix, and you can check how your Plan is doing, day or night, with the app or on the website. If you have any questions about Plan(s) or investing in general, don’t hesitate to contact us on 0800 802 1800 or via Live Chat.

*‘Simulated’ returns are so named as they are based on the performance of a model which identically mirrors the decisions we take on customers’ Plans. It is based on an account size that is over £500 and assumes that our maximum Wealthify fee (0.70% from 2016 to December 2019 and 0.60% from December 2019) is taken, as well as underlying fund costs. Individual customer returns may deviate slightly from the model figures, particularly those customers who may have added to or withdrawn from their Plans throughout the year or have a different fee rate.

References:

1: Fool - FTSE 100: these were the five most critical days for UK investors in 2020

2: Data from Bloomberg

Past performance is not a reliable indicator of future results.

The tax treatment depends on your individual circumstances and may be subject to change in the future.

Please remember the value of your investments can go down as well as up, and you could get back less than invested.