Please note: this blog was published in December 2020 and its content is based on what was correct at the time of writing. As a result, some of the facts and opinions may no longer be current or relevant.

When it comes to investing, there are two main ways you can build wealth. The first is that you buy when prices are low, and sell when they're higher.

The price in between what you bought your investment for and what you sold it for is your profit, and shows 'asset appreciation' in action.

The second way is that your investment pays out an income, and if you’re investing in companies, this potential income is known as a 'dividend'.

Here’s a short guide to help you understand how dividends work.

What are dividends?

Put very simply, dividends are payments made by a company to its shareholders. Dividends can be distributed annually, semi-annually or quarterly and are paid from the company’s profits or their reserves (think of it like the company’s savings).

The amount you receive is entirely up to the company’s board of directors and depends on the proportion of company you own – the more you own, the greater the dividend you can expect to receive.

What are the different types of dividends?

There are different types of dividends, and as an investor it’s important to know the varying kinds of dividend payments.

The main categories are cash dividends and stock dividends, and as the names imply, the first type is simply a payment made in cash whilst stock dividends allocate you additional shares in the company which you can keep, increasing the size of your shareholding, or sell for cash if you wish.

Another type of dividend is the preferred dividend, and it’s linked to the type of stock you hold. If you hold preferred stock, or preference shares, you will receive your payments before shareholders with common stock, or ordinary shares.

One thing to note though is that all shareholders, without exception, will get their payments after bondholders have been paid their principal by the company.

Now, say the company you’re investing in has a particularly good quarter. If the business wanted to, it could choose to pay a special dividend – these are like bonuses paid on top of your dividends and they’re usually a one-time payment, hence the name. Special dividends are normally paid out in cash and will typically be larger than your regular dividends.

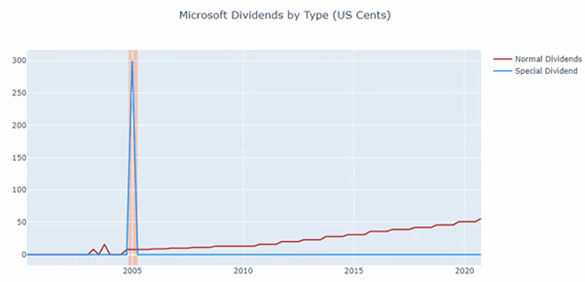

For instance, Microsoft has steadily increased its quarterly dividend since the start of 2005 from 8 cents per share to 56 cents quarterly (chart below).

However, this is still well below the 300 cents special dividend that Microsoft paid back in December 2004. Obviously, there is no guarantee that Microsoft will continue to increase its dividend like this, but this shows how fruitful special dividends can be.

Are dividends guaranteed payments?

Good question! And the answer is no. A company has no legal obligation to pay dividends to its shareholders. So, if one year, the company is struggling financially, for example, it could decide to stop distributing dividends until the outlook improves.

In this case, the company may also decide to reduce its dividend payments, and depending on the type of shares you hold, you may get nothing those years. Remember, bondholders get paid first, then preferred shareholders can receive their payments, and it's only after that common stockholders can get their due, if there’s anything left for them.

How are dividends taxed?

Since dividends are a form of income, you may need to pay income tax on your earnings – it all depends on how much you’ve been paid. Typically, you only need to pay tax on any dividend income that exceeds your dividend allowance, which is currently set at £2,000 per tax year (subject to change).

This means you can earn up to £2,000 in dividends tax-free – the rest may be subject to tax. How much tax you pay on dividends will depend on your Income Tax band.

Let’s use an example to illustrate. If you receive £3,000 in dividends and earn £29,500 in the current tax year, then your total income would be £32,500. Every tax year, you can enjoy a Personal Allowance of £12,500 (subject to change).

This means you will only pay income tax on the income that sits above this threshold – for more information about income tax and your Personal Allowance, check out the HMRC website.

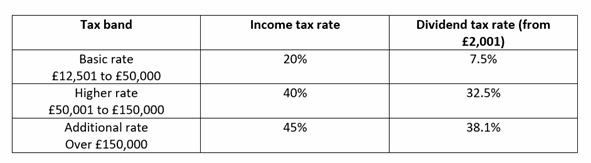

So, here you could expect to pay income tax on £20,000, and with this income, you’d fall into the basic rate where your wages get taxed 20% and your dividends get taxed 7.5%. As a result, you could be paying 20% on £17,000 (your total income minus dividends) and 7.5% on £1,000 (your taxable dividends).

Here’s a table that sums it up for you (assuming you are a tax resident in Northern Ireland, Wales or England). If you are fortunate enough to live in Scotland the numbers are slightly different.

Paying into a Stocks and Shares ISA allows you to invest tax-efficiently. With a Stocks & Shares ISA, or Investment ISA, you won’t need to pay any tax on your investment earnings, and you’ll be able to keep more of your profits. ISAs come with some rules and it’s worth knowing them.

The total amount you can put in a Stocks and Shares ISA is limited to £20,000 per tax year – this is your ISA allowance. And you have until midnight the 5th April to use it for that tax year, or you’ll lose it forever.

What could you do with your dividends?

What you do with your dividends is up to you. You could either decide to take the cash income payments and spend them on anything you like, or you could choose to put them back into your investment plan and wait for them to potentially generate further returns in the future.

If you were to re-invest your dividends every time you get them, your pot could grow exponentially bigger over time – this phenomenon is called ‘compounding’ and if you want to make the most of your investment journey, it could pay off to take advantage of it.

At Wealthify, we will wherever possible use accumulation funds – think of them as hampers full of investments. These funds are designed to automatically reinvest any profits that companies distribute, in other words, their focus is on growth, not income.

If you’re pursuing long-term growth and want to enjoy the magic of compounding, investing in accumulation funds could help.

But if you don’t feel confident enough to choose your own funds, then why not use an online investment platform, like Wealthify? The sign-up process is easy. You choose how much you want to invest and how much risk you want to take, then we’ll do the rest and build you a portfolio with the right mix of funds.

The tax treatment depends on your individual circumstances and may be subject to change in the future.

With investing your capital is at risk, the value of your investments can go down as well as up, and you could get back less than invested.

Past performance is not a reliable indicator of future results.

Wealthify does not provide financial advice. Please seek financial advice if you are unsure about investing.

References:

1. Data from Bloomberg.