Let’s start with a little bit of background to what a ‘benchmark’ is. The term benchmark originated in the land surveying profession in the 19th century, and then referred to a point of reference that was carved into stone, so that levelling rods could be repeatedly and accurately be repositioned1. The concept of a ‘benchmark’ is used across many disciplines today and is typically related to measurement.

When applied to investments, benchmarks are used to assess investment manager performance. Essentially, the benchmark’s performance, or returns over a specified investment period, provides a reference point to understand how a particular investment has performed comparatively. While this may sound simple, the different types of investments make understanding the nuances of benchmarking an important aspect of assessing performance, which is a vital part of selecting the best investments.

Here, we’ll cover the main aspects to give you a better understanding of your investment performance.

What are the different types of benchmarks?

There are four main types of benchmarks:

- Index-based – the main type of benchmark we encounter with our managers in Wealthify Plans.

- Peer Group – we use this type of benchmark for our Plans.

- Measure-based

- Absolute

Index-based benchmarks

Index-based benchmarks mirror the performance of a collection of investments – for us, this is typically shares or bonds. Indexes are constructed based on a set of rules that decide what investments make up the list and in what proportion. For example, we have an index bringing together the 100 largest UK companies – the FTSE 100 Index. Now, you might ask how is ‘large’ determined? Essentially, the size of a company is decided by the market-based price of each share, which determines the value of the total shares. This makes up the ‘size’ of the company in the index, and as the share price changes, companies will trade places in terms of being larger or smaller, and some companies may drop out and be replaced entirely based on market movements. Of course, we have many other types of indexes, with some tracking bonds for example, or have different rules to weight members. Index-based benchmarks are what we mostly encounter when looking at funds that focus on either shares or bonds.

Peer group benchmarks

Peer group benchmarks are another type of benchmark that is commonly seen. This is when investors are grouped together, and the performance of the group is averaged to provide a benchmark of the collective. Each investor in the group can then compare their performance to the average to determine how they fared amongst peers. These benchmarks are more common in funds that hold a variety of different types of assets, such as share and bonds. They are also more common investments that are made up of funds, like our Plans at Wealthify.

Measure-based benchmarks

The third type of benchmark is one that is linked to a particular measure, for example, inflation or a cash rate at a bank. These are typically used for investments in cash, or cash equivalents, or cautious investments where cash and other very low risk investments form the bulk of the portfolio. For example, the Wealthify Original Cautious Plan uses an inflation-based benchmark owing to its low-risk status.

Absolute benchmarks

Closely related to the above, are absolute or fixed benchmarks. These are less common but are essentially benchmarks that have a stated return outcome, such as 8% compounding over 3 years. What is more common is to see a combination of measure-based and absolute. These benchmarks are more common in funds that hold a variety of different types of assets, such as shares and bonds. They are also more common investments that are made up of funds, like our Plans at Wealthify.

Time Horizons

One thing to mention with benchmarks is the time horizon. Often a fund’s objective of outperforming the benchmark will be stated as annually, but it is to be achieved over say a 3-to-5-year period (these longer time horizons are indicative of higher exposure to risk assets such as shares, that may take longer to pay off and experience greater ups and downs in terms of price). Of course, this makes sense as there may be one year where the investment has a bad year, followed by two very good years, thereby achieving its stated goal.

Let us look at an example.

Table 1: Investment v Benchmark Performance (using hypothetical data)

* Please note that the above table has been designed for illustrative purposes only and the returns used are hypothetical.

As can be seen in the above, the investment underperforms in its first year as the benchmark rises nicely. In the subsequent years, the investment outperforms to such an extent that if we smooth the returns over the three years, the investment outperforms annually on a three-year basis. A little bit confusing, but this illustrates the point that it can be a good idea to stay the course and be wary of judging an investment on short-term performance, particularly when the objective of the investment stipulates a longer time horizon, which is a fancy name for investment period. Please remember that this is only an example using hypothetical performance and is not based on Wealthify or real world data. Now in graph form…

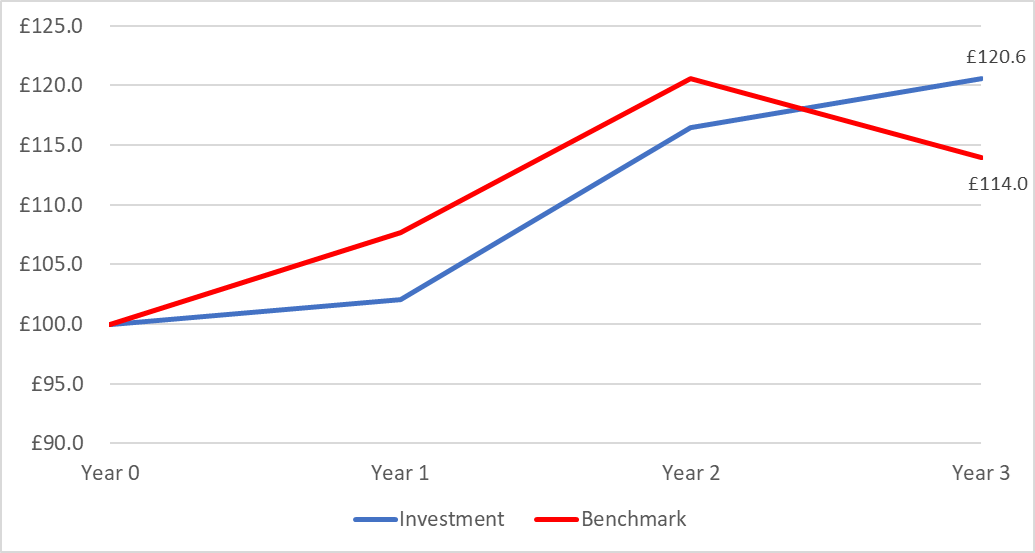

Graph 1: Investment v Benchmark Performance (using hypothetical data)

*Please note that the above graph has been designed for illustrative purposes only and the returns used are hypothetical.

As we see from the above, if we started at £100 of our investment, we would have £120.6 at the end of three years, while if we held the benchmark we would only have £114.0. Crucially, we see that the outperformance is only generated in year 3 of the investment when the benchmark is negative, and the investment does very well. Please remember that this is only an example using hypothetical performance and is not based on Wealthify or real world data.

Another point this example raises, is understanding the performance of your investment. A crucial part of our fund research process at Wealthify is understanding what drives the performance of our fund managers, so that we know what to expect in different market environments and from the fund managers’ process. Insight into this allows us to gain confidence that over longer-term periods our investments will outperform, but maybe not all at the same exact time.

The Role of Benchmark in Passive Investments

The main role of the benchmark in passively managed funds, is to provide a target for performance replication. Passive or tracker funds, which are used mainly in the Wealthify Original Plans, seek to track the performance of a chosen index using various replication strategies. The easiest to understand of these replication strategies, is direct replication. In this method, the manager purchases the investments exactly as they are represented in the index, which leads to direct performance replication before fees. We mainly use the benchmark as a relative measure to assess how well the manager can track the chosen index.

The Role of Benchmark in Active Investments

The main role of benchmarks in actively managed funds used in our Ethical Plans is to provide a way to assess the performance of the fund. Our active fund managers choice of benchmark signals the broad collection of investments that they are aiming to outperform after fees. Of course, this is the job of active managers (and why we pay higher fees for them) – they must outperform the benchmark to justify their purchase over that of a passive investment that tracks the same benchmark.

What are we looking for in a benchmark?

There is a very useful acronym for the ideal benchmark characteristics – SAMURAI - which stands for:

Specified in advance: The benchmark should always be specified before the measurement period begins; else it could be chosen to suit the result, which would not be useful.

Appropriate: The benchmark should reflect the manager’s investment style and area of competence.

Measurable: The benchmark’s returns should be easy to calculate frequently.

Unambiguous: The benchmark must have clear definition in terms of weights and the underlying investments.

Reflective: The manager must have current knowledge of the investments in the benchmark.

Accountable: The manager accepts accountability for the performance of the investments that make up the benchmark.

Investable: Investors can hold the benchmark if they wish (i.e., investors can buy the benchmark as an alternative).1

At Wealthify, we typically segment the global share market into geographical regions and at the most granular level, countries, where appropriate. We then look for funds that specialise in these areas. With many of the funds we invest in following index-based benchmarks, most of the desirable qualities of benchmarks, such as ‘Measurable’, are automatically satisfied. Therefore, we focus more on selected characteristics depending on the type of investment…

In our Original Plans, we are looking for funds that target benchmarks that represent a particular region or country’s business environment by providing exposure to a range of shares and sectors, thereby reducing concentration in any one or group of shares. We are also looking for benchmarks that are relatively easy for the managers to replicate and track, as this gives us the performance we expect and reduces costs.

In our Ethical Plans, it is most important that a fund’s benchmark reflects the broad range of shares that can be chosen from (Appropriate), and that there is a passive product we can purchase that mirrors the benchmark (Investable). This ensures that we are targeting the correct investments and that we can measure the performance of the manager against the benchmark and alternative passive investments to assess their value add.

Wrapping up

Benchmarks are important to investors as they provide a way to evaluate the performance of passive and active investments. In passive investing, the benchmark is mostly used to assess how well the manager can track the chosen index after fees; while in active investing, we are looking for outperformance of an appropriate and investable benchmark over appropriate time periods. Most of the funds in Wealthify Plans use index-based benchmarks, which have a range of desirable qualities, such as typically being investable. This said, the sheer amount of indexes - there are over 5000 indexes for US shares alone2 – means that it is important to understand the benchmark of each investment and ensure that it is a suitable benchmark for the strategy in question. Only then, do we have a chance at meaningfully evaluating performance and in turn selecting top performing investments.

References

2: https://www.bloomberg.com/news/articles/2017-05-12/there-are-now-more-indexes-than-stocks

Past performance is not a reliable indicator of future results.

Please remember the value of your investments can go down as well as up, and you could get back less than invested.