Money is something that impacts all our lives, yet many people don’t have the knowledge they need to manage it with confidence and make good financial decisions.

So, we wanted to see just how financially savvy the nation is. To get a better idea, we teamed up with the economic thinktank, CEBR, to create a new Financial Literacy Benchmark – the first ever barometer to measure financial literacy across the country.

We quizzed 2,250 Britons on their understanding of 10 frequently discussed financial topics – including inflation, taxes, pensions, and savings – to gauge knowledge across different age groups and regions.1

To get a good pass rate, respondents needed to achieve a score of at least 6.5 out of 10.

So: how did they do? The answer may surprise you.

And if you want to see how your financial knowhow measures up against the rest of the UK, you can take the quiz we used in this research at the end of this blog.

What were the results?

Our research found that almost three quarters (73%) of the country actually fall below this benchmark, exposing the UK as a weak performer on financial literacy when compared to other similarly developed countries, like France, Canada, and New Zealand.

Despite needing to achieve a score of 6.5 or above, 73% fell below the new benchmark, and just 1 in 20 (5%) answered all 10 questions correctly. And it seems that young people are most lacking in financial knowledge with the average 16–18-year-olds getting just 2 questions right.

The results also showed that there was a strong link between financial understanding and behaviours, with 7 out of 10 respondents with the highest level of financial literacy contributing to a pension to save for their future. 13% of individuals at the top of the benchmark scale also had a significantly higher savings rate than those in bottom.

Sam Miley, Senior Economist at CEBR comments:

“This research reveals considerable divergence in financial understanding amongst the UK population and between generations. We have also found a strong association between such understanding and the prevalence of positive financial behaviours, such as saving, contributing to a pension, and avoiding risky payment mechanisms.

“This suggests that those lacking financial literacy could be at a disadvantage when it comes to their financial health. This point is made all the more pertinent given the difficulties faced by many households amidst the ongoing cost-of-living crisis.”

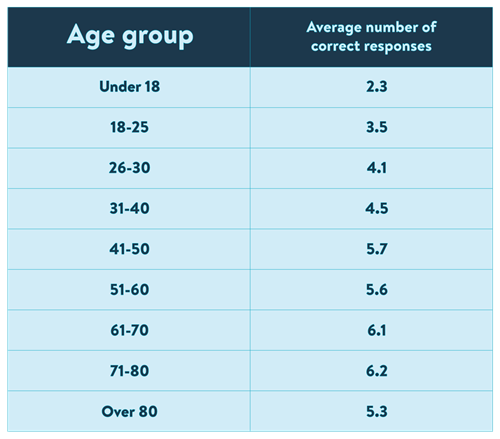

Young people scored the lowest in terms of Financial Literacy

With the average score across all ages already below the threshold for financial literacy (a score of 6.5), the report also exposed a stark gap between young people (aged 16-18), and older respondents (aged 71-80), as it was found that the older age group averaged 6.2 correct responses, compared to just 2.3 amongst those aged between 16 and 18.

Only 46% of 16-18-year-olds were able to correctly answer questions about the impact of inflation on savings, and only 36% of under 18s answered questions about mortgages correctly.

Here’s a clearer picture of how each age group scored:

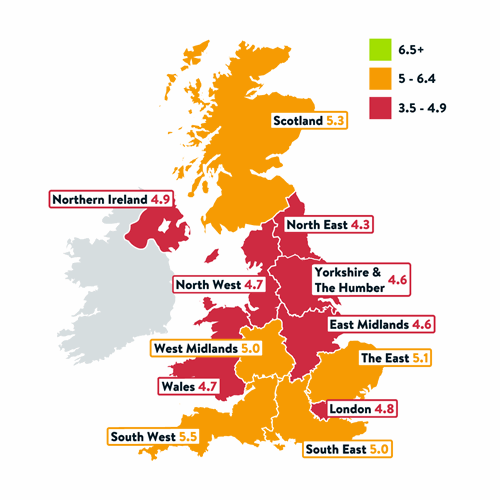

How do levels of financial literacy differ by region?

On a regional basis, the highest number of correct answers was reported amongst respondents in the South-West, where people scored 5.5 on average.

At the other end, the lowest average score was in the North-East, where the average was just 4.3 correct responses – and it was found that they scored particularly poorly on questions about inflation and investing.

Here’s a breakdown of the average score by region of the UK:

So, where do we go from here?

Having sufficient financial education in school could help build better saving habits and a healthy relationship with money in future – but it’s something that doesn’t always get the attention it deserves.

And as our research shows, there’s a clear lack of financial literacy amongst young people in the UK – those who will soon be managing their own money as they head off to university or enter the world of work and earn money for the first time.

Wealthify really wants to make a difference in this area, so, to help young people gain a better understanding of financial matters, we’ll be joining forces with the charity, Young Enterprise, to provide free financial education resources in schools in September 2023.

Here’s what our Chief Executive Officer, Andy Russell, has to say about the results of our research and this upcoming partnership:

“The results of our inaugural Financial Literacy Benchmark assessment with CEBR show 16 and 17-year-olds lack vital knowledge about day-to-day finance. These are essential skills, especially as many of them are about to become financially independent for the first time, in a tough economic environment. It is a critical time in any person’s life, when they first have an opportunity to establish healthy money habits of their own and build confidence in financial decisions that can last a lifetime; something made even more challenging by the current cost of living crisis.

“The findings show a clear association between age, exposure to monetary decisions and choices over time, and levels of financial literacy. This suggests that earlier introduction to real-world financial decision-making could have a positive impact on young peoples’ long-term outlook. However, teachers have told us they lack the confidence and resources to cover these topics with young people. That is why we are working with financial and enterprise education charity, Young Enterprise, to launch free financial education tools in schools this September, designed to help 16 to 18-year-olds get to grips with essential monetary know-how, just as they reach financial maturity.”

Sharon Davies, CEO of Young Enterprise, also adds:

“The new benchmark from Wealthify and CEBR offers important fresh insight into the poor state of financial literacy across the UK population – particularly among young people – and how that links to financial behaviour. Young people and students rank lowest for financial literacy. That lack of knowledge has a hugely detrimental effect on their financial health – with real consequences for the rest of their lives.

“The current cost of living crisis and move towards a more cashless society only increases the need to provide young people with a solid financial education. Any investment to improve young people’s financial literacy not only pays huge dividends to their lives, but their families, communities, and wider society.”

Reference

- Research conducted on behalf of Wealthify by CEBR in 2023

Take the quiz to see if you score higher than the Financial Literacy Benchmark

Remember, you’ll need to achieve a score of 6.5 to be above the Benchmark. And don’t forget to make a note of your answers so you can check they’re correct at the end!

The questions:

1. In the UK, in which month does a new tax year begin? This is also referred to as a fiscal year.

a. January

b. February

c. March

d. April

e. May

f. June

g. July

h. August

i. September

j. October

k. November

l. December

m. Don’t know

2. Imagine you earn £60,000 per year. In this case your marginal income tax rate would be 40%. In this situation, how much of your income is lost to tax each year?

a. Less than 40%

b. Exactly 40%

c. More than 40%

d. Need more information

e. Don’t know

3. Suppose you have £100 in a savings account earning 2% interest per year. After five years without making any deposits or withdrawals, how much would you have in the account?

a. More than £110

b. Exactly £110

c. Less than £110

d. Need more information

e. Don’t know

4. Suppose you are offered an interest rate on a savings account of 5% but can choose how frequently interest is paid into the account. Any interest paid into this account would also receive interest (compound interest). Assuming you don’t make any deposits or withdrawals, which of the following would leave you with the largest value in the account after two years?

a. Interest paid annually

b. Interest paid every six months

c. Interest paid quarterly / every three months

d. Interest paid monthly

e. It would not make a difference

f. Need more information

g. Don’t know

5. Imagine that the interest rate on your savings account is 2% per year and inflation is 4% per year. After two years, would the money in the account buy more, exactly the same, or less than it does today?

a. More

b. Same

c. Less

d. Need more information

e. Don’t know

6. Imagine you are buying apples. Which of the following represents the best deal in terms of price per apple?

a. Six apples for £5

b. Twelve apples for £9

c. One apple for £1

d. Two apples for £3

e. Need more information

f. Don’t know

7. Suppose inflation in April was 5.0% and that inflation in May was 4.0%. How did prices change between April and May?

a. Prices were higher in April than May

b. Prices were lower in April than May

c. Prices were the same in April and May

d. Need more information

e. Don’t know

8. Imagine you have a variable rate mortgage. Which of the following will lead to the amount you pay each month changing?

a. The amount of money you earned that month

b. Changes in the Bank of England’s interest rate / base rate

c. Fluctuations in the value of your property that month

d. The amount you need to spend on other goods and services that month

e. Need more information

f. Don’t know

9. If your investment increased in value by 8% in 2021 and a further 8% in 2022, by how much would its value increase in 2023?

a. More than 8%

b. Exactly 8%

c. Less than 8%

d. Cannot be certain

e. Need more information

f. Don’t know

10.Which of the following will NOT affect your credit score?

a. Being registered to vote

b. Missing a payment on an existing debt

c. Checking your existing credit score

d. Making regular payments by direct debit

e. Need more information

f. Don’t know

The answers:

1. D (April)

2. A (less than 40%)

3. A (more than £110)

4. D (interest paid monthly)

5. C (less)

6. B (twelve apples for £9)

7. D (need more information)

8. B (changes in the Bank of England’s interest rate / base rate)

9. D (cannot be certain)

10. C (checking your existing credit score)