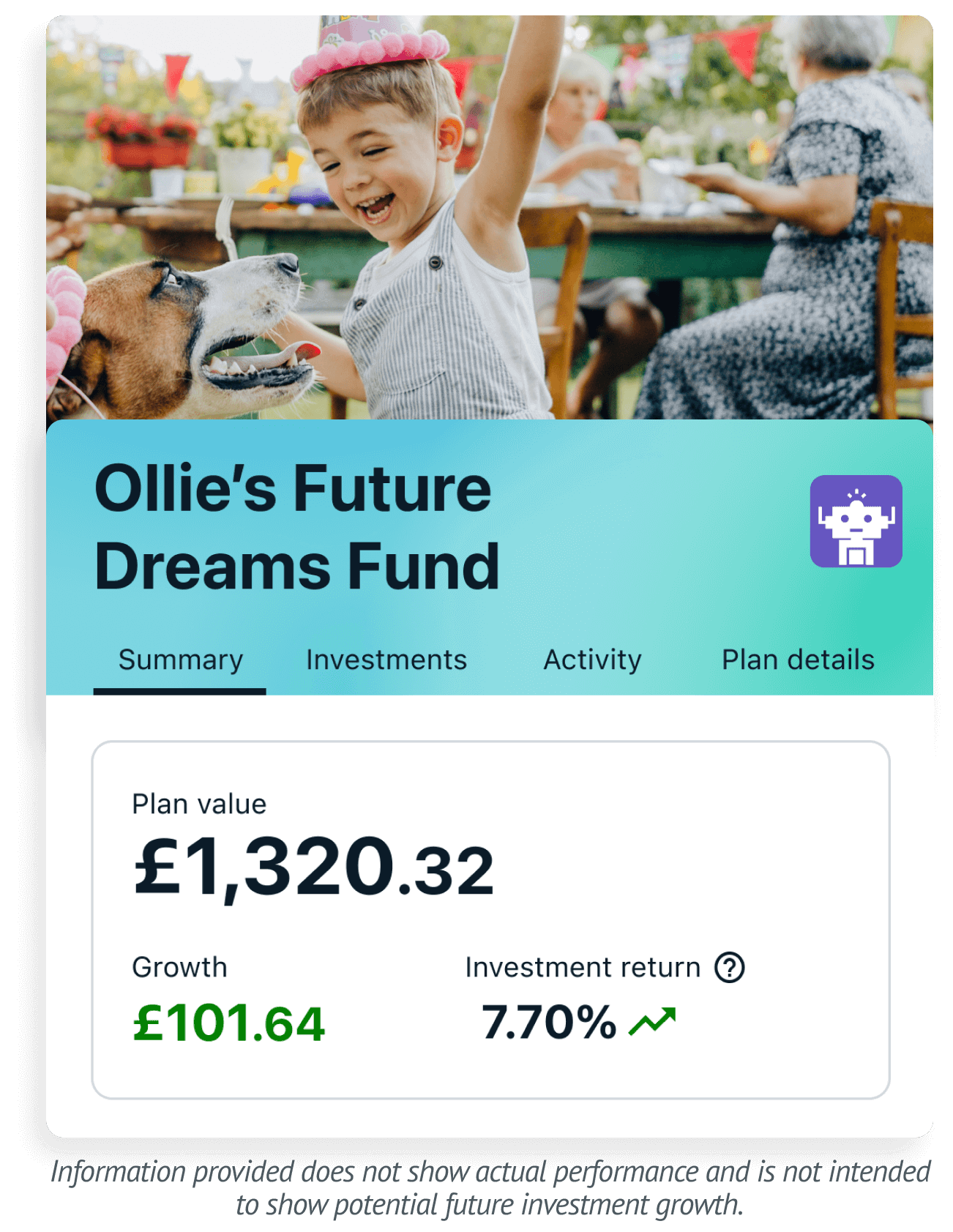

Ethical Junior ISA

We don’t think investing should cost the earth. That’s why our Ethical Junior Stocks & Shares ISA (JISA) helps you:

✓ Limit your child's money being invested in harmful industries and activities.

✓ Invest in organisations which are aware of their impact on Environmental, Social, and Governance (ESG) concerns.

✓ Keep more of your child's money invested, thanks to our low fees.

With investing, your capital is at risk. The tax treatment of your investment will depend on your individual circumstances and may change in the future. Minimum deposit of £500 required.

Best Junior ISA - 7 years running

Personal Finance Awards

How to start an Ethical Junior isa

Choose your plan

Pick from 5 investment styles from Cautious to Adventurous, and tell us how much you want to invest for your child via a one-off payment or Direct Debit.

Answer our quiz

This is our way of helping you start your child's JISA in a way that's right for your circumstances and attitude to risk.

We build and manage your Plan

Our experts then get to work on building and managing your child's Plan, keeping it in line with your chosen style.

Access to the JISA

Your child will have access to their JISA on their 18th birthday, at which point the money can be used as they see fit — including reinvesting it, potentially.

What is ethical investing?

Ethical investing is an investment strategy that considers both financial returns and wanting to invest in line with your values.

At Wealthify, we invest in funds which focus on the ESG credentials of their chosen companies. As a result, our Ethical Plans aim to exclude industries and activities that are considered harmful to society and the environment, including:

- Tobacco

- Gambling

- Controversial weapons

- Adult entertainment

Whether from a moral, religious, or social standpoint, one of the biggest motivations for investing ethically is being able to grow wealth in a way that aligns with your values.

The fund providers we use have a 10% (maximum) tolerance when they screen for excluded activities.

How ethical investing works

We've joined forces with best-in-class ethical fund providers to create five Ethical Plans.

All our fund providers are signatories of the Principles of Responsible Investing (PRI), the world’s leading proponent of responsible investing. With the actively managed ethical funds in our Plans, a close eye is kept on the organisations in which they invest through rigorous, ongoing screening to ensure ethical standards are maintained.

Our approach to making your money work ethically can be divided into two sections: investing and optimising.

We invest

The fund providers we use have a 10% (maximum) tolerance when they screen for excluded activities. This means we can’t guarantee that Plans won’t contain some degree of exposure to the harmful activities listed.

Rest assured, however, that these funds are actively managed, and we will de-invest in funds that fail to meet these high standards.

We optimise

Once your Ethical Plan is up and running, our Investment Team then regularly reviews it.

They do this for two reasons: to help keep your Plan’s performance on track — and to make sure your money’s invested as ethically as possible.

With investing, your capital is at risk. The tax treatment of your investment will depend on your individual circumstances and may change in the future.

Transfer To Our Junior ISA

If you want to give your Junior Cash ISA or Child Trust Fund more potential, we've made transferring them to Wealthify's Junior Stocks and Shares ISA a simple, hassle-free process.

Just let us know you want to move to Wealthify, then we'll do the rest. If you're looking to move an existing Junior Stocks and Shares ISA or Child Trust Fund, please note that we'll need to move the whole amount, as you're only allowed one account of this type per child.

Invite contributors

When it comes to raising a child, there's nothing quite like a helping hand.

Which is why – whether it's family, friends, or that lovely lady next door – our Junior ISA lets you invite anyone to contribute towards and grow your child's savings.

They can even leave a personalised note for every contribution they make, creating that memorable touch.

Ethical guide

If you want to learn more about ethical investing and its significance, we've created a comprehensive guide to help you explore how it works, ways to invest ethically, key considerations, and much more.

This guide doesn't offer personal advice, speak to a financial adviser if you're unsure about whether investing is right for you.

Wealthify Customer Reviews

Junior ISA FAQs

A Junior ISA is a tax-efficient way to save and invest on behalf of your child.

Payments into a Junior ISA are different from adult ISAs, because the money you put in belongs to your child. Once you put money in, you can’t take it out again, except in exceptional circumstances, and your child can only get access to their money when they turn 18.

There are two types of Junior ISA:

- Junior Cash ISAs: earn interest like a savings account. The interest rate is fixed and typically based on the rate set by the Bank of England.

- Junior Stocks & Shares ISAs: (Also known as Junior Investment ISAs), these invest in financial markets with the aim of earning returns for investors that are greater than those you would get in a Junior Cash ISA. Returns are not guaranteed, and the value of your investments can go down as well as up.

Your child can have one or both types of Junior ISA and you can deposit up to the annual limit of £9,000 into them in any combination you like.

For example, you could pay £3,000 into a Junior Cash ISA and up to £6,000 into a Junior Stocks and Shares ISA, or vice versa. You can split the allowance however you want to between the two accounts.

The benefit of a Junior ISA is that you or your child won’t pay tax on any interest, returns or dividends they receive.

Wealthify only offers a Junior Stocks and Shares ISA. Any money paid into a Junior ISA will belong to the child, but they cannot access it until their 18th birthday.

Ethical Investing aims to exclude profiting from activities that are considered harmful to society and the environment and to invest in organisations, companies and projects that are committed to operating in a way that is sustainable for the future.

This is typically done by filtering out harmful activities (negative screening) and proactively seeking to invest in companies that are committed to making a positive impact through their environmental, social and governance (ESG) practices (positive screening).

Negative screening: most ethical funds will screen the so-called ‘sin stocks’ such as tobacco, gambling, weapons and adult entertainment. Other issues screened might include animal testing, intensive farming, nuclear power, genetic engineering, deforestation, and poor human or labour rights. The activities screened and the screening criteria used, vary between fund providers.

Positive screening: aims to identify those companies demonstrating or showing commitment to achieve the highest standards of practice in the areas of environmental impact, social justice and corporate ethics. Only organisations that score highly across these three areas will be eligible to receive investors’ money.

Wealthify’s ethical plans combine negative screening with proactive selection based on ESG scores, as well as qualitative, human consideration of a wide range of other factors that contribute to a commitment to future sustainability.

Ethical investing is one of a number of terms used to identify sustainable approaches to investing. Others include Environmental, Social and Governance (ESG), Sustainable Investing and Impact Investing.

If you want to build an investment pot for your child that neither you or they can touch until your child turns 18, then a Junior ISA could be the answer. Any money paid into a Junior ISA belongs to the child and cannot be withdrawn by anyone other than the child when they turn 18.

Junior ISAs are available to children who:

- Are under the age of 18

- Are residents of the UK, or are dependants of a crown employee (e.g. army employee based overseas)

- And don’t already have a Child Trust Fund (CTF).

You can transfer your Child Trust Fund over to a Wealthify Junior ISA, but your child cannot have a CTF and a Junior ISA at the same time. When transferring a CTF to a Junior ISA, the full balance must be transferred.

Our Ethical Plans are built using mutual funds. The funds contain multiple investments, selected by the fund providers according to their strict ethical screening processes.

The funds will typically include:

Shares (owning a piece of a company): excluding companies that profit from ‘sin sectors’ such as gambling, tobacco, adult entertainment and weapons among others. It will only include companies that demonstrate great environmental, social and governance standards, according to the fund providers’ and Wealthify’s strict criteria and ethical investing policies.

Bonds (an IOU from a government or company with some interest): both corporate and government bonds may be included and will be subject to the same strict screening criteria as shares.

Thematic investments: one or two funds will focus on investing themes such as gender equality (companies that strongly champion these issues) or green energy and will mostly be used in higher risk plans.

We’ve created five Ethical Investment Plans – from Cautious to Adventurous – so you can choose a level of risk that’s right for you. Find out more about what’s in each of these plans by downloading the ethical plan factsheets, below.

Ethical Plan Factsheets

Cautious Ethical Plan [download pdf]

Tentative Ethical Plan [download pdf]

Confident Ethical Plan [download pdf]

Ambitious Ethical Plan [download pdf]

Adventurous Ethical Plan [download pdf]

Money added to a Junior ISA belongs to the child. The parent or guardian who opened the Junior ISA acts as the registered contact, but they can’t access the money once it has been deposited, unless there are exceptional circumstances. When the child turns 18, account ownership is transferred to them.

We’re using best-in-class ethical fund providers: Edentree, Pictet, Liontrust, Royal London, Stewart Investors, Brown Advisory, and Rathbone. They have been selected for their exemplary quality of governance and ethical stance, and each employ rigorous and ongoing screening processes to ensure appropriate ethical credentials for the relevant funds.

All of the ethical fund providers we use are signatories of the Principles of Responsible Investing (PRI), the world’s leading proponent of responsible investing. The PRI is an independent body acting in the long-term interests of its signatories, of the financial markets and economies in which they operate and ultimately of the environment and society as a whole. More information: about the PRI.

A Junior ISA allows you to save or invest up to £9,000 a year on behalf of your child without paying tax on any interest and/or capital gains earnt from the money within the Junior ISA.

Saving into a Junior ISA on behalf of your children does not affect your own annual ISA allowance.

Fund providers will typically exercise two levels of screening:

Negative screening: aiming to exclude companies involved in activities that are at odds with ethical and socially responsible values. This typically means ‘sin stocks’ such as gambling, tobacco, adult entertainment and weapons, although most funds screen many more activities besides.

Positive screening: actively seeking and investing in companies that demonstrate excellent environmental, social and governance (ESG) practices. More about what this means can be found in What is ESG, sustainable and Impact investing? Fund providers will employ a scoring system to each company, rating it against a set of predefined criteria, such as energy efficiency, equality agenda and the quality of its corporate governance, looking at, for example, whether it has been fined in the past for regulatory violations. These all add up to an ESG rating, which determines whether a company should be considered for investment. Our ethical funds don’t just invest in companies with the highest ESG ratings. They will also identify and invest in ‘improving companies’ – i.e. those that show significant commitment to improving their environmental, social and governance practices. An example might be a coal company that is investing a significant part of its profits in the research and development of green energy.

Looking for support?

Our Customer Care team are always there to help, whether you have a question about your Wealthify Plan, you’re having trouble with the app, or you’re simply unsure of how to get started when it comes to investing with us. Whatever you need, just get in touch.

Telephone

Lines are open Monday - Friday, 8.00am - 5.30pm

Live Chat

Chat to one of our team online.