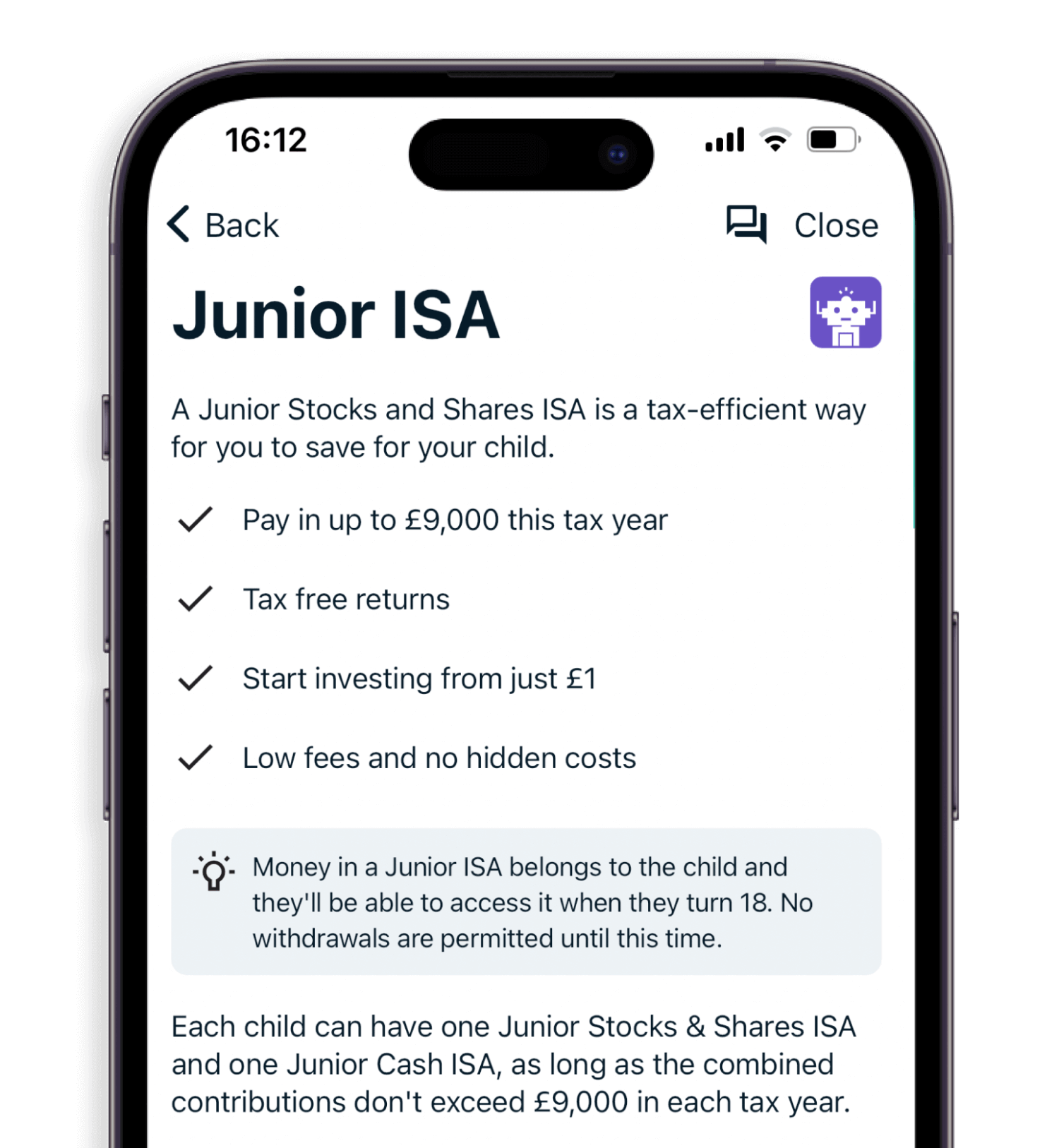

Junior Stocks and Shares ISA

Invest in Wealthify's award-winning Junior ISA. Our Junior ISA means:

- A tax-efficient way to save up to £9,000 every year for your child.

- More of your child's money stays invested, thanks to our low-transparent fees

- Staying true to your values, thanks to our Ethical Junior ISA option.

With investing, your capital is at risk. The tax treatment of your investment will depend on your individual circumstances and may change in the future.

Best Junior ISA - 6 years running

Personal Finance Awards

Why choose a Junior ISA for your savings?

With a Junior ISA – also known as a JISA – you can save and invest without being taxed on the interest or gains. This is especially important because, if the money saved for your child generates more than £100 in interest a year, it'll be taxed at the parent's tax rate for all the interest — not just the bit that's over £100.

A Junior ISA protects against this, with all interest and gains being tax-free meaning they get to keep more of their returns. And, seeing as their profits are reinvested to try and generate further profit (known as compounding), their Junior ISA could grow a bit faster.

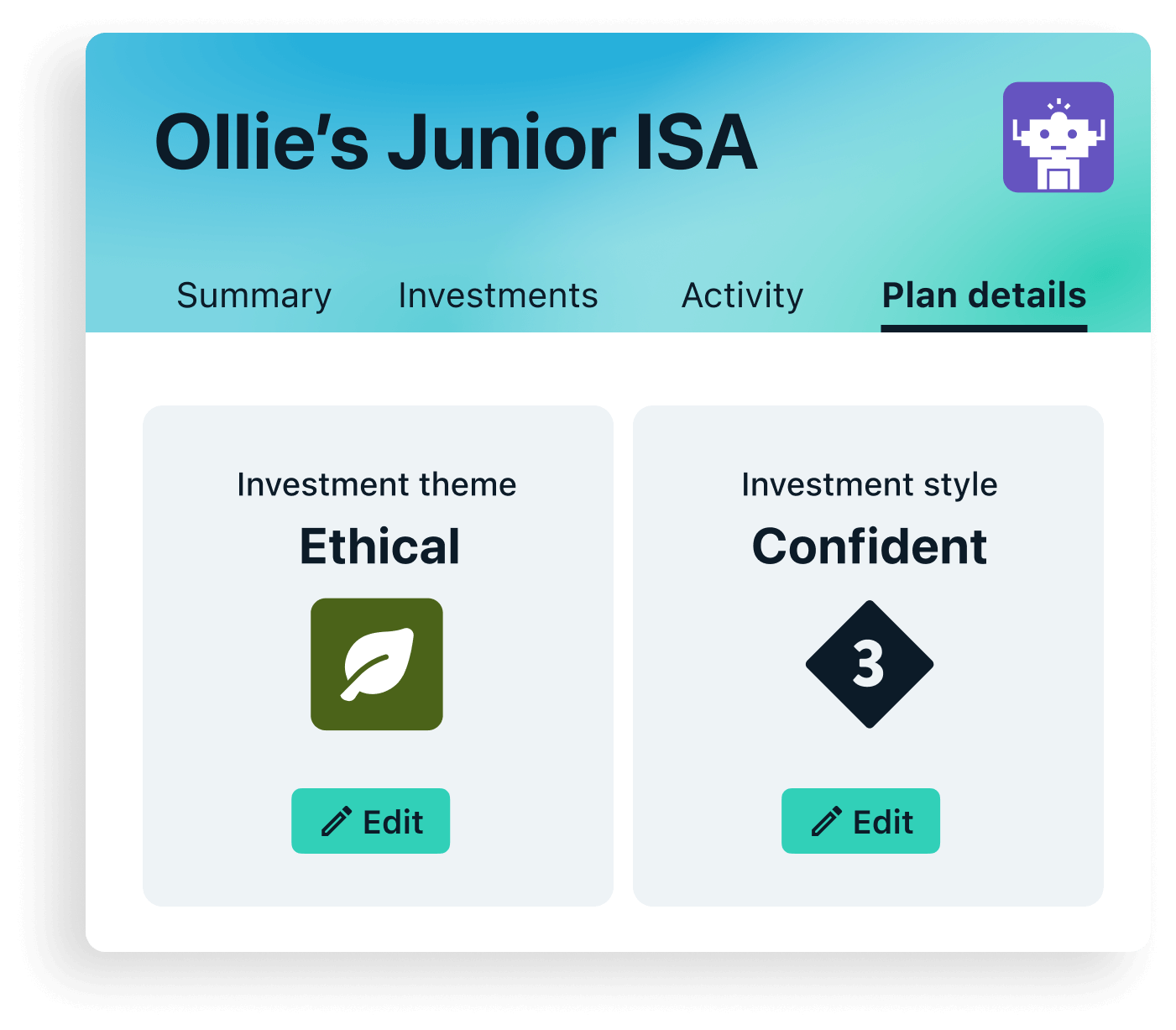

Ethical Junior ISA investment options

Help shape a sustainable future for your child

- Invest up to £9,000 tax efficiently each year and give their money a chance to make a difference.

- Wealthify's Ethical Plans aim to exclude industries and activities that are considered harmful to society and the environment such as unfair labour practices and deforestation.

- With actively managed ethical funds, the activities of the companies your child's money is invested in are regularly monitored.

- Learn more and stay up-to-date with our Ethical Blogs

How to start a Junior isa

Choose your plan

Pick from 5 investment styles, our Original or Ethical Plan, and tell us how much you want to invest for your child via a one-off payment or regular Direct Debit.

Take our Suitability Quiz

This is our way of helping you start your child's JISA in a way that's right for your circumstances and attitude to risk.

We build and manage your Plan

Our experts then get to work on building and managing your child's Plan, keeping it in line with your chosen style.

Access to the JISA

Your child will have access to their JISA on their 18th birthday, at which point the money can be used as they see fit — including reinvesting it, potentially.

Transfer to a Wealthify Junior ISA

If you want to give your Junior Cash ISA or Child Trust Fund more potential, we've made transferring them to Wealthify's Junior Stocks and Shares ISA a simple, hassle-free process.

Just let us know you want to move to Wealthify, then we'll do the rest. If you're looking to move an existing Junior Stocks and Shares ISA or Child Trust Fund, please note that we'll need to move the whole amount, as you're only allowed one account of this type per child.

Friends and family

When it comes to raising a child, there's nothing quite like a helping hand.

Which is why – whether it's family, friends, or that lovely lady next door – our Junior ISA lets you invite anyone to contribute towards and grow your child's savings.

They can even leave a personalised note for every contribution they make, creating that memorable touch.

Wealthify: a name you can trust

Secure

Your login details will always be kept secure — but never shared with anybody else.

Supported

Strength

Wealthify is owned and backed by Aviva: one of the UK's largest financial institutions.

Free Junior ISA guide

Junior ISAs come with a set of rules from HMRC, and there are different types you can open. In this useful Junior ISA guide, you'll find out:

- The difference between a Junior Cash ISA and Junior Stocks and Shares ISA

- How much you can pay into a Junior ISA

- How many Junior ISA accounts you can open

- How to transfer a Junior ISA

What is the Junior ISA Allowance?

The Junior ISA allowance for this tax year is

£9,000

Wealthify Customer Reviews

Junior ISA FAQs

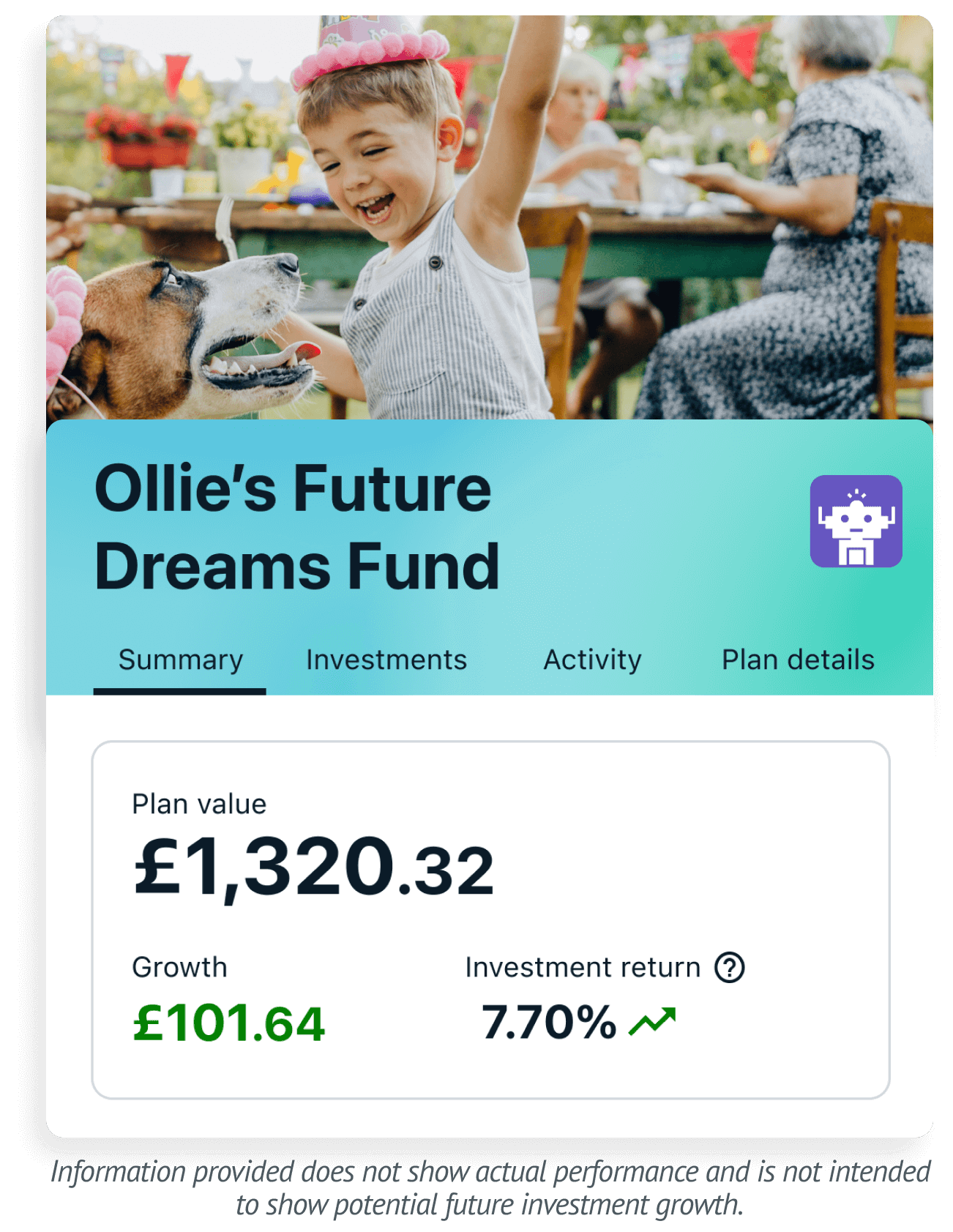

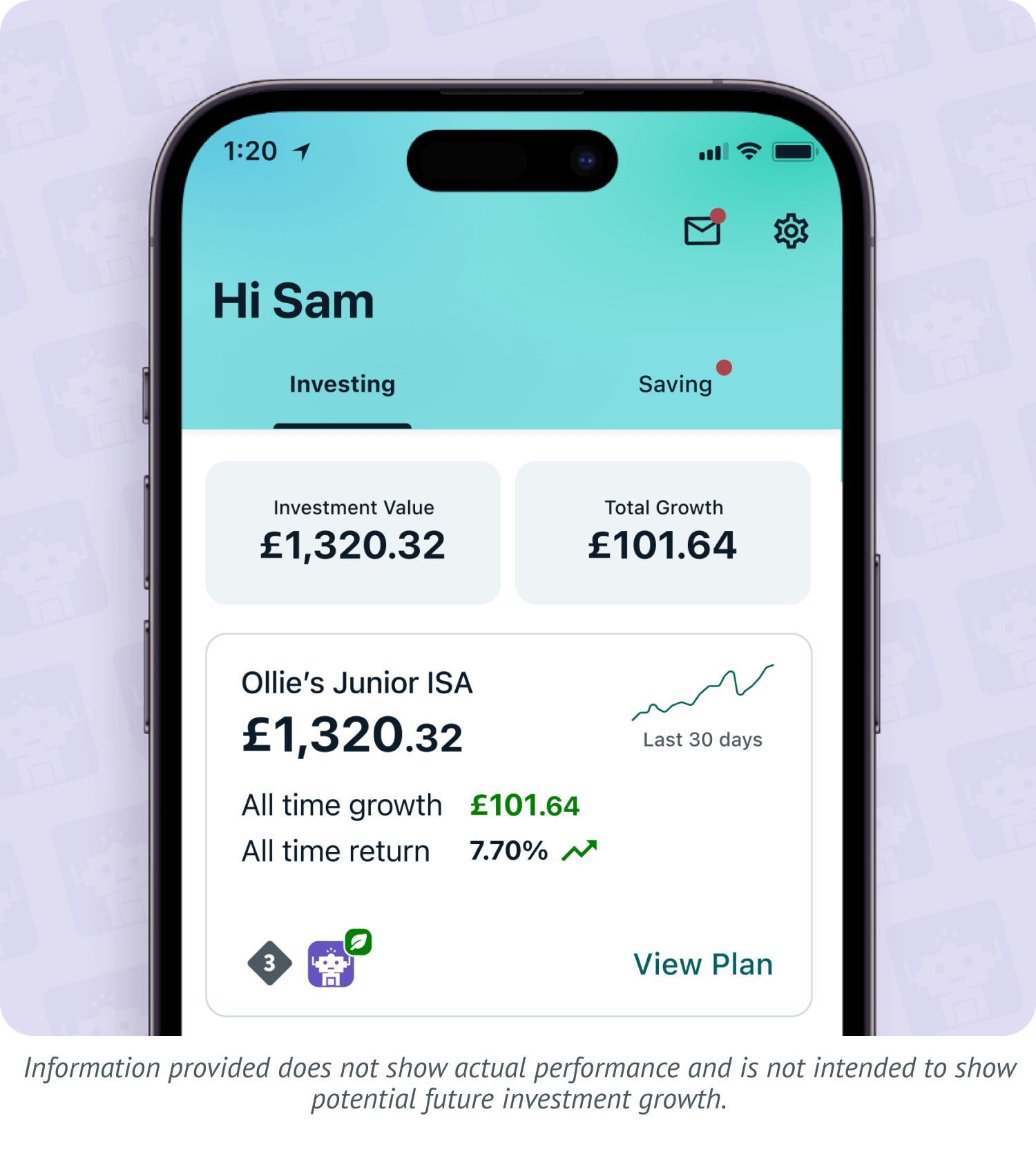

A Junior ISA is a tax-efficient way to save and invest on behalf of your child.

Payments into a Junior ISA are different from adult ISAs, because the money you put in belongs to your child. Once you put money in, you can’t take it out again, except in exceptional circumstances, and your child can only get access to their money when they turn 18.

There are two types of Junior ISA:

- Junior Cash ISAs: earn interest like a savings account. The interest rate is fixed and typically based on the rate set by the Bank of England.

- Junior Stocks & Shares ISAs: (Also known as Junior Investment ISAs), these invest in financial markets with the aim of earning returns for investors that are greater than those you would get in a Junior Cash ISA. Returns are not guaranteed, and the value of your investments can go down as well as up.

Your child can have one or both types of Junior ISA and you can deposit up to the annual limit of £9,000 into them in any combination you like.

For example, you could pay £3,000 into a Junior Cash ISA and up to £6,000 into a Junior Stocks and Shares ISA, or vice versa. You can split the allowance however you want to between the two accounts.

The benefit of a Junior ISA is that you or your child won’t pay tax on any interest, returns or dividends they receive.

Wealthify only offers a Junior Stocks and Shares ISA. Any money paid into a Junior ISA will belong to the child, but they cannot access it until their 18th birthday.

Junior ISAs allow your child to keep more of their money by protecting any positive returns they receive from income tax and capital gains tax.

Only a child’s parent or legal guardian can open a Junior ISA account on their behalf.

Your child can have one Junior Cash ISA and/or a Junior Stocks and Shares ISA at any time, into which you can currently contribute a maximum of £9,000 per tax year, per eligible child. You can split the amount however you choose between a Junior Cash ISA and a Junior Stocks and Shares ISA as long as the combined amount doesn’t exceed the annual limit.

You don’t need to use the same provider for your child’s Junior Cash ISA and Junior Stocks and Shares ISA, so you’ve got flexibility to choose the best option for you and your child.

At the start of each new tax year, on 6 April, the child’s annual Junior ISA allowance re-sets and you can start another year of tax-efficient saving for each child.

Your child will only be able to access the money within their Junior ISA when they turn 18.

When they turn 18, the Junior ISA is automatically changed into an adult ISA. At this point, they can choose to keep saving or investing, or they can withdraw some or all of the balance to help pay for things like university, or a new car.

If you want to build an investment pot for your child that neither you or they can touch until your child turns 18, then a Junior ISA could be the answer. Any money paid into a Junior ISA belongs to the child and cannot be withdrawn by anyone other than the child when they turn 18.

Junior ISAs are available to children who:

- Are under the age of 18

- Are residents of the UK, or are dependants of a crown employee (e.g. army employee based overseas)

- And don’t already have a Child Trust Fund (CTF).

You can transfer your Child Trust Fund over to a Wealthify Junior ISA, but your child cannot have a CTF and a Junior ISA at the same time. When transferring a CTF to a Junior ISA, the full balance must be transferred.

Junior ISAs can only be opened by the parent or legal guardian of a child under the age of 18 who fits the eligibility criteria. Once opened the parent/guardian will become the registered contact for the account.

As the registered contact for a Junior ISA, you are the only person authorised to make decisions about the management of the account. You’ll also need to keep Wealthify informed if the child’s personal details change; e.g. if they change their name, address, contact number, or get married.

When the child turns 18, they will become the registered contact and their Wealthify Junior ISA will change into an adult ISA. They can either keep investing, move it somewhere else, or withdraw some or all of it e.g. to help pay for university, or a car.

The money in a Junior ISA will never belong to the parent/guardian. It belongs to the child, but they won’t be able to access it until their 18th birthday.

Wealthify offers Junior Stocks & Shares ISAs.

Wealthify Junior ISAs contain a range of investments from across the globe matched to the level of risk you choose. Our team of experts build your child’s Junior ISA, choosing which investments to buy and managing them on your behalf.

You can choose to invest for you child in an Ethical Plan or an Original Plan. Read more about our Ethical Plans here.

Each Junior Stocks & Shares ISA will contain up to 20 investment funds from providers like Blackrock and Vanguard. Investment funds are a convenient and cost-effective way to invest, as they contain hundreds or even thousands of expertly-selected shares, bonds and other investment types. This means your Junior ISA will contain a diverse range of investments spread across global markets and regions, helping your child to spread their risk.

Yes, you can invite anyone to be a contributor. That could be your parents, siblings, cousins, friends, neighbours… the list goes on. Once they’ve accepted the invite, and passed verification, they’ll be able to add to your child’s ISA whenever they want.

The only caveat to this is that they’ll need to live in the UK and be a UK tax resident, aged over 18.

You can invite someone to pay into your Wealthify Junior ISA by using our 'Friends and Family' feature. You can find out more about this here: Junior ISA family friends.